[1] Sam Walker, “Average pension pot by age”, Money Week, n.d., accessed 6 February 2026. (link)

[2] Office for National Statistics, “Chapter 6: Private pension wealth, Wealth in Great Britain, 2012 to 2014, 18 December 2015. (link)

[3] Based on 8% vs 9% annualised returns. 8% delivers a total future investment value of £523,651. (9% delivers a total future investment value of £702,198. (monthly compound frequency)

[4] “Aviva study reveals critical knowledge gap about UK pensions”, Aviva, 22 April 2025. (link)

[5] The Investment Association, “Investment Management Survey 2022-23”, ch. 4 UK Institutional Market, October 2023. (link)

[6] S.P. Kothari, “Why Shareholder Wealth Maximization Despite Other Objectives”, Harvard Law School Forum on Corporate Governance, 23 May 2018. (link)

[7] The Global Compact, Who Cares Wins: Connecting Financial Markets to a Changing World, 2004. (link)

[8] Thomas P. Fitch, Dictionary of Banking Terms, 2nd ed. (New York: Barron’s, 1990), 244.

[9] Chaim Saiman, “Fiduciary Principles in Classical Jewish Law” in The Oxford Handbook of Fiduciary Law, ed. Evan J. Criddle, Paul B. Miller, Robert H. Sitkoff (Oxford: Oxford University Press, 2019), Chaim Saiman, 560.

[10] The renowned seventeenth century biblical commentator Matthew Henry summarised the significance of the financial meaning of this passage: “such a reputation [the temple workmen] got for honesty that there was no occasion to examine their bills or audit their accounts. Let all that are entrusted with public money, or public work, learn hence to deal faithfully, as those that know God will reckon with them, whether men do or no. Those that think it is no sin to cheat the government, cheat the country, or cheat the church, will be of another mind when God shall set their sins in order before them…. [Let us] whence we may learn, in all our expenses to give that the preference which is most needful, and, in dealing for the public, to deal as we would for ourselves” Matthew Henry’s Complete Commentary on the Bible. (link)

[11] Stephen M. Bainbridge, “The Parable of the Talents”, Law and Economics Research Paper Series, no. 16-10, 2 June 2016. (link)

[12] “The Twelve Tables” in Ancient Roman Statutes, trans. Allan Chester Johnson, Paul Robinson Coleman-Norton, Frank Card Bourne (Austin: University of Texas Press, 1961). (link)

[13] Cicero, De Officiis I.23

[14] Klaus Schwab and Peter Vanham, “What is stakeholder capitalism?”, World Economic Forum, n.d. (link)

[15] Andrew Pudzer, A Tyranny for the Good of Its Victims: The Ugly Truth About Stakeholder Capitalism (New York: Encounter Books, 2024), 2.

[16] “ESG Being Dropped From Corporate Sustainability Report Titles”, Carrier Management, 29 April 2025. (link)

[17] United Nations, “Secretary-General launches ‘principles for responsible investment’ backed by world’s largest investors”, press release, 27 April 2006. (link)

[18] Glasgow Financial Alliance for Net Zero, n.d. (link)

[19] FCA, “The Financial Conduct Authority’s Adaptation Report”, January 2025. (link)

[20] HM Government, “Mobilising green investment: 2023 green finance strategy”, GOV.UK, 11 April 2023. (link).

[21] GFANZ, “Call to Action: One Year On”, 2022. (link)

[22] Legal & General, “L&G sets Lifetime Advantage Funds as new default strategy for contract-based DC clients”, 17 December 2024. (link)

[23] Legal & General, “L&G Climate Action Global Equity Fund, n.d. (link)

[24] Moira O’Neill, “Beware of wealth managers quoting data”, Financial Times, 17 Augustu 2023. (link)

[25] Benjamin Graham, The Intelligent Investor: The Definitive Book on Value Investing, 3rd ed., (New York: Harper Business, 2024), 505.

[26] BlackRock, “A Sense of Purpose: Larry Fink’s Annual Letter to CEOs”, 2018. (link)

[27] BlackRock, Annual Stewardship Report 2020, September 2020, 10. (link)

[28] BlackRock, “BlackRock in the UK”. (link)

[29] Legal & General, “Climate and nature report 2024” (2024), 2. (link).

[30] CFA Society United Kingdom, “Case study: Implementing responsible investing at Scottish Widows”, n.d. (link)

[31] Scottish Widows, “Investments”, n.d. (link)

[32] The Investment Association, “Our Position on Climate Change”, n.d. (link)

[33] John Crabb, “Forget greenwashing, the real problem is ‘greensmuggling’”, Global Capital, 14 October 2022. (link)

[34] Royal London, Climate Transition Plan, 26 June 2025. (link)

[35] Royal London, “Climate Transition Plan”, 26 June 2025, 1. (link)

[36] Milton Friedman, “A Friedman doctrine—The Social Responsibility of Business Is to increase Its Profits”, The New York Times, 13 September 1970. (link)

[37] Companies Act 2006, 172.1.d. (link)

[38] Companies Act 2006, 172.1.

[39] Wellington Management, “Building a solid foundation: The latest steps in our net-zero journey”, n.d. (link)

[40] AstraZeneca, “Annual Report & Form 20-F 2000”, 2001, 7. (link)

[41] AstraZeneca, “What science can do: Annual Report and Form 20-F Information 2024”, 2025. (link)

[42] AstraZeneca, “Climate change”, May 2025. (link)

[43] Vinay Prasnad and Sham Mailankody, “Research and Development Spending to Bring a Single Cancer Drug to Market and Revenues After Approval”, JAMA Internal Medicine, 177(11):1569–1575. doi:10.1001/jamainternmed.2017.3601. (link)

[44] Prasnad and Mailankody, “Research and Development”.

[45] KnowESG, “AstraZeneca PLC: ESG & Sustainability Profile”, n.d. (link)

[46] Iman Zalinyan, “The ESG Dilemma in the Pharmaceutical Industry: Balancing Innovation, Ethics, and Sustainability”, RSM, n.d. (link)

[47] Greenhouse Gas Protocol, “Scope 3 Calculation Guidance”, n.d. (link)

[48] Green Element Group, “Carbon Footprint: Simplifying Scope 1, 2 & 3”, 26 October 2018. (link)

[49] IEA, “United Kingdom”, n.d. (link)

[50] Stephen Jones, “Sainsbury’s opens eighth wind farm site in renewable energy push”, The Grocer, 15 October 2024. (link)

[51] J Sainsbury PLC, “Wind in the sails: Eighth wind farm now helping to power Sainsbury’s”, 16 October 2024. (link)

[52] Jonathan Brocklebank, “Wind farms funded by Amazon and Tesco help at £1.5bn to YOUR bill”, The Daily Mail, 22 March 2024. (link)

[53] Fidelity International, “Why invest with us”, 30 September 2025. (link)

[54] Fidelity International, “Our net zero commitment”, n.d. (link)

[55] Tesco, “Tesco and NatWest join forces to help farmers reduce costs and decarbonise”, 28 March 2024. (link)

[56] NatWest, “Finance Options for your Ambitions” n.d. (link)

[57] Total farming subsidy in the UK is £3.025 million, the total number of farms is 209,000, hence an average subsidy per farm of £14,500. See Department for Environment, Food & Rural Affairs, “Total income from farming in the UK in 2024”, 5 June 2025. (link)

[58] Tesco, “Making a positive impact: Tesco PLC Sustainability Report 2024/25”, 2025,12. (link)

[59] Tesco, “Agriculture”, n.d. (link)

[60] Siân Yates, “Controversy erupts over Bovaer feed additive trial in UK dairy industry”, Foodbev, 6 December 2024. (link)

[61] ADHB, “England’s cattle and sheep populations his record lows: Beef and lamb market update”, Thursday 4 September 2025. (link)

[62] Green Alliance, “English farmers are at risk of being left behind in tackling methane emissions”, briefing, August 2024. (link)

[63] Business New Wales, “Collaboration Tackles Carbon Emissions in Wales’ Food & Drink Industry”, 20 March 2025. (link)

[64] Schroders Capital, “ESG”, n.d. (link)

[65] Schroders, “Our UK clients”, n.d. (link).

[66] This reference is technically in relation to Schroders as opposed to Schroders Capital (the private asset management arm); however, it seems reasonable to assume that most if not all of these will be invested by Schroders in capital strategies. See Schroders, “Schroders Capital awarded £500 million private equity mandate by Wales Pension Partnership. (link)

[67] Fatima Benkhaled, “Scottish Widows to invest in companies driving decarbonisation”, Pensions Expert, 3 February 2022. (link)

[68] LGPS, “Facts and figures”, n.d. (link)

[69] Border to Coast, “Homepage”, n.d. (link)

[70] London CIV, “London CIV Climate Change Policy”, n.d. (link)

[71] Columbia Business School, “One Key Corporate Challenge to Going Green: Rethinking the Cost of Capital”, press release, 25 June 2025. (link)

[72] Niels Joachim Gormsen, Kilian Huber, and Sangmin S. Oh, “Climate Capitalists”, SSRN, 22 February 2023, 2. (link)

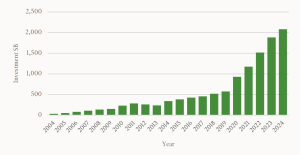

[73] BloombergNEF, Global Investment in Energy Transition, by Sector, 2004-2024 (Abridged report), 30 January 2025. (link)

[74] iShares Global Clean Energy ETF (link); Legal & General, “L&G Clean Energy Units ETF”, n.d. (link)

[75] Rupert Darwall, It’s Broke, Fix It: Where British Energy Policy Went Wrong and How to Get It Right (London: Prosperity Institute, 2026), 9. (liznk)

[76] UK Parliament, “Debate on transitional support for North Sea oil and gas workers”, research briefing, 22 April 2025. (link)

[77] Rian Chad Whitton, Destroying the Foundations: How Net Zero Could Wreck British Industry for Good (London: Prosperity Institute, 2025), 29.

[78] Whitton, Destroying the Foundations, 8.

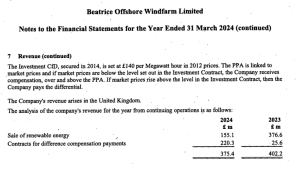

[79] Department for Energy Security and Net Zero, “Contracts for Difference (CfD) Allocation Round 7: results”, 14 January 2026. (link)

[80] Trading Economics, “United Kingdom Electricity Price”, accessed 11 February 2025. (link)

[81] Companies House, “Beatrice Offshore Windfarm Limited: Annual Report and Financial Statements for the Year Ended 31 March 2024”, posted 24 September 2024, 15. (link)

[82] Nestlé, “What is Nestlé doing to tackle packaging waste?”, n.d. (link)

[83] Legal & General, “Ethnic diversity: Financially material, social imperative”, 2020, 3. (link)

[84]Legal & General, “Ethnic diversity”, 9.

[85] GOV.UK, “Population of England and Wales”, 22 December 2022. (link)

[86] Legal & General, “Ethnic diversity”, 6.

[87] Paradigm, “What is DEI? The Meaning of Equity and Inclusion in the UK”, 26 January 2026. (link)

[88] Who Cares Wins, 6

[89] United Nations, “The 17 Goals”, n.d. (link)

[90] Fidelity International, “Sustainable Investing Principles”, July 2024, 16. (link)

[91] Fidelity, “Together we can be more FutureWise”, 2025, 3, 9. (link)

[92] UNCDF, “Financial Inclusion and the SDGs”, n.d. (link)

[93] https://uk.investing.com/equities/unilever-ord-ownership

[94] https://www.unilever.com/sustainability/equity-diversity-and-inclusion/transforming-our-brands-transforming-our-advertising/#:~:text=issues%20such%20as%20racial%20discrimination%2C%20equal%20rights%20and%20social%20justice.

[95] “Dylan Mulvaney Bud Light Commercial Original”, YouTube, 14 April 2023. (link)

[96] Sarah Taaffe-Maguire, “Dylan Mulvaney: Bud Light beer takes sales hit after backlash over ad campaign featuring transgender influencer”, Sky News, 3 August 2023. (link)

[97] Danielle Kaye, “Michelob Ultra becomes best-selling beer in the US”, BBC, September 2025. (link)

[98] Soo Yun, “Nike sales booming after Colin Kaepernick ad, invalidating critics”, ABC News, 21 December 2018. (link)

[99] Schroders, “Schroder Sustainable Multi-Factor Equity Fund”, March 2025. (link)

[100] Rolls Royce, “Share price”, accessed 11 February 2026. (link)

[101] BAE Systems, “Share price monitor”, accessed 11 February 2026. (link)

[102] Babcock, “Share Price Centre”, accessed 11 February 2026. (link)

[103] Sylvia Pfeifer, “Class UK defence investments as ethical, Labour MPs urge banks”, Financial Times, 6 March 2025. (link)

[104] James Graham, “Parliamentary pensions’ punishment of defence” The Critic, 15 April 2025. (link)

[105] James Graham, “How pensions are disarming Britain”, The Critic, 5 January 2026. (link)

[106] Quoted Companies Alliances, “The never-ending story of annual reports”, n.d. (link)

[107] Fidelity International, “What are the main approaches to ESG?”, n.d. (link)

[108] Sam Chambers and Jill Treanor, “JD Sports blasted over ‘inappropriate’ bonuses for chairman Peter Cogwill”, The Times, 13 June 2021. (link)

[109] Sarah Butler, “JD Sports owner’s profits soar thanks to US shoppers spending stimulus checks”, The Guardian, 14 September 2021. (link)

[110] Legal & General, “How we’re working toward our net zero emissions target”, 3 July 2023. (link)

[111] Rachel Millard, “BP faces shareholder backlash over U-turn on green strategy”, Financial Times, 11 April 2025. (link)

[112] Glass Lewis, “About us”, n.d.(link)

[113] Glass Lewis, “ESG Profile Methodology”, n.d. (link)

[114] Glass Lewis, “About us”.

[115] Glass Lewis, “Thematic Policies Overview”. (link)